February 2026 Market Overview

February saw renewed volatility as investors reassessed AI-driven valuations, growing disruption risks, and the pace at which heavy capital spending will translate into returns, triggering sharp selloffs in parts of the technology sector. US CPI came in softer than expected, lifting rate-cut expectations, while Q4 GDP undershot forecasts, with much of the weakness attributed to the temporary government shutdown rather than underlying demand. A Supreme Court decision tied to former President Trump’s trade powers introduced fresh uncertainty around tariff policy. In South Africa, the national budget was viewed as fiscally credible, with the rand strengthening and local assets moving higher. Geopolitical tensions intensified at month end after US and Israeli strikes on Iran, adding a further layer of uncertainty heading into March.

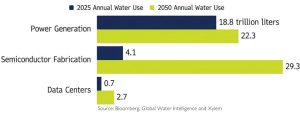

AI’s Water Demand

The AI buildout is often discussed in terms of power demand, but water is emerging as a parallel constraint. The majority of future water demand linked to AI does not stem directly from data centres, but from power generation and semiconductor fabrication. While data centres consume significant water for cooling, more than half of their water footprint is tied to upstream electricity production, particularly when fossil fuels are involved. Semiconductor manufacturing is even more water intensive, with demand projected to rise sharply as chip complexity increases. In calm conditions this dynamic attracts limited attention, but in water-stressed regions the combination of rapid AI expansion and local resource constraints could create friction between industry, communities and regulators.

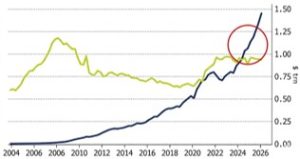

The Case for Caution in Credit Markets

Corporate credit markets appear stable, but underlying fragility has increased. Spreads are near historic lows while liquidity has weakened, raising the risk that any selloff could become sharp and disorderly. As the chart illustrates, traditional liquidity providers such as banks and dealers have reduced their balance sheet exposure, while liquidity-dependent investors, including ETFs and bond funds, now dominate corporate bond holdings. This shift has created a liquidity mismatch that is largely invisible in calm markets, but during periods of stress there may be fewer natural buyers to absorb selling pressure. As a result, credit markets are vulnerable to abrupt repricing should risk sentiment deteriorate.

Credit Default Swaps

US CDS jumped sharply in February, climbing to around 84 from 63 at the end of January, while European CDS rose to roughly 59 from 54. The move was gradual early in the month but accelerated noticeably toward month end, alongside growing discussion of structural liquidity risks in corporate credit markets. Higher borrowing costs and signs of pressure in parts of the US credit market further weighed on sentiment. Together, these factors drove increased hedging activity and a clear shift to a more defensive risk backdrop into month end.

Performance

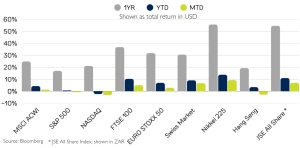

Performance diverged meaningfully in February following a broadly positive January. The US lagged, with the Nasdaq declining 3.3% for the month, pushing its year-to-date return into negative territory. In contrast, Europe and the UK extended their gains, while Japan stood out, rallying close to 10% after Prime Minister Sanae Takaichi’s election win. The JSE All Share also delivered a strong performance, advancing 7% in February.

Volatility picked up in February, reflecting higher short-term market sensitivity. US equity volatility increased meaningfully, with 30-day volatility rising to 13.5% for the S&P 500 and 18.1% for the Nasdaq. Volatility also moved higher in Japan, Hong Kong and South Africa, with the Nikkei 225 and JSE All Share recording notable increases in 30-day measures. European markets were comparatively more stable, with volatility either broadly unchanged or only modestly higher.