January 2026 Market Overview

January was an eventful and chaotic month, with sharp daily moves, noisy headlines and shifting narratives. A steady stream of geopolitical and policy headlines, including renewed focus on Venezuela and Greenland, added to the noise alongside protests in Iran. US CPI data came in modestly softer, while central bank meetings from the Federal Reserve, Bank of Japan and SARB all resulted in rates being left unchanged. At the same time, speculation around Fed leadership, including the selection of Kevin Warsh, weighed on sentiment and pushed the US dollar to its weakest level since September. Precious metals also experienced a sharp pullback, underscoring the uneven and rapid repricing seen across asset classes.

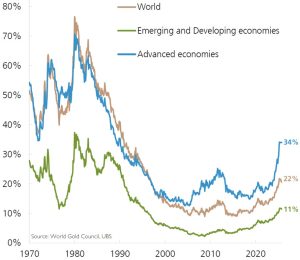

Central Bank Gold Reserve as % of total Reserve

The longer-term structural theme is growing central bank demand for gold, reflecting diversification away from traditional reserve assets and a hedge against geopolitical and fiscal uncertainty. While gold experienced a sharp pullback earlier in the month, this underscored the volatility that can accompany elevated precious metals prices even as structural demand remains intact.

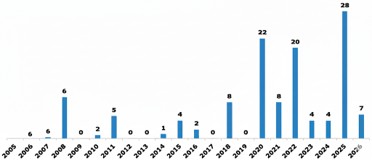

Rising Frequency of High-Volume Trading Days

The frequency of exceptionally high-volume trading days has risen sharply, with 2025 standing out for an unusually large number of sessions where the SPDR S&P 500 ETF (SPY) turnover exceeded $60 billion, a pattern that has already repeated seven times in early 2026. This elevated trading intensity has coincided with an unforgiving earnings season, during which individual shares have seen large and often abrupt price reactions alongside exceptionally high trading volumes, reflecting heightened sensitivity to even small earnings surprises and forward-looking guidance.

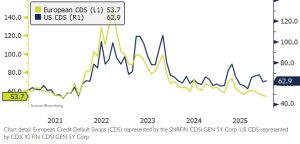

Credit Default Swaps

Credit markets remained relatively stable through January, with only a modest pickup in credit spreads. US CDS spreads remain elevated following the pickup seen in September, indicating a continued degree of caution in US credit markets. In contrast, European CDS spreads have remained relatively low compared to recent stress periods.

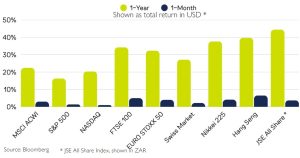

Performance

Despite sharp day-to-day moves in individual shares that made January feel more volatile than the month-end index returns suggest, global equity indices delivered broadly positive returns, building on the strong performance seen in December. Gains were led by European and Asian markets, which posted returns of between 4% and 7% (in USD terms) for the month, while US equities continued to trail global peers, with more modest gains of 1.4% for the S&P 500 and 1.0% for the NASDAQ.

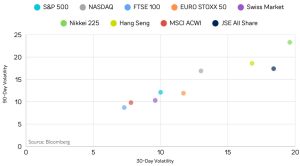

While January felt turbulent at times, volatility remained relatively contained across indices. 30-day volatility in US equities declined despite ongoing market noise, while European markets, together with the JSE All Share, experienced a pickup in 30-day volatility.