March 2026 Market Overview

March was shaped by a sharp escalation in geopolitical tensions, with the conflict in the Middle East driving significant moves across financial markets. Oil prices rose materially amid supply disruptions, rising by approximately 63% to end the month at around $118 per barrel, while gold declined by almost 12% to close at approximately $4,668 per ounce. The Federal Reserve has adopted a cautious, wait-and-see stance, with market expectations shifting meaningfully as rate cuts for 2026 have largely been priced out and the probability of policy remaining on hold has increased. Notably, both equities and bonds declined, reflecting the inflationary nature of the shock, while the US dollar strengthened, reinforcing its role as a safe-haven. Private credit markets have also come into focus, with early signs of tighter liquidity conditions and rising uncertainty beginning to surface.

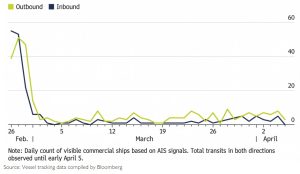

From Open Passage to Negotiated Access

Shipping through the Strait of Hormuz fell sharply, with traffic reduced to a fraction of normal levels.. Given that approximately 20% of global oil supply transits through the strait, the disruption has had significant implications for global energy markets. A total of 21 vessels transited the strait over the weekend of 5-6 April, the highest two-day total since early March, with access increasingly dependent on countries negotiating directly with Iran, further reinforcing its control over the waterway. Access is now determined less by maritime convention and more by country-specific agreements.

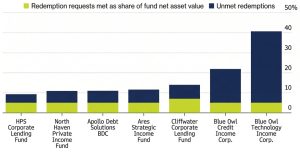

Rising Pressure in Private Credit Markets

Private credit markets have come under increasing scrutiny, as elevated redemption requests begin to test the liquidity structure of the asset class. As illustrated above, investors have sought to withdraw record amounts, with requests in some funds exceeding 20%–40% of assets, far above typical quarterly limits of around 5%, leaving a meaningful portion of capital effectively locked up. More importantly, this has intensified concerns among regulators and market participants around the potential for broader systemic risk, particularly if liquidity pressures begin to spill over into other parts of the financial system. Together, this highlights a key structural feature of private credit, where inherently illiquid assets are paired with more flexible investor liquidity expectations.

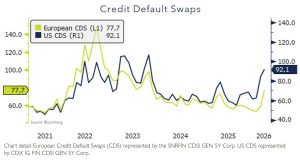

Credit Default Swaps

Credit spreads widened through March, reflecting a deterioration in risk sentiment. US CDS rose from 84 to 92, while European CDS increased more sharply from 59 to 78. The larger move in Europe points to greater sensitivity to the recent escalation in geopolitical tensions and the associated energy shock, given the region’s closer economic exposure. Overall, the rise in CDS levels reflects a more cautious environment, as investors reassess credit risk in the context of higher inflation expectations, tighter financial conditions, and increased uncertainty around the growth outlook.

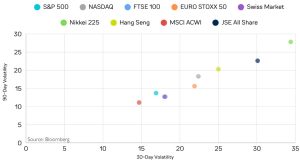

Performance

We saw broad-based declines across most major indices, with weakness most pronounced in Japan, Europe, and South Africa. In the US, both the S&P 500 and NASDAQ Composite declined, although the drawdowns were more contained relative to other regions. Notably, much of the positive year-to-date performance seen at the end of February was erased during March, leaving several indices in negative territory for the year.

Volatility picked up meaningfully across all major indices. By the end of March, volatility levels were highest in Japan and South Africa. The move higher was particularly sharp across Europe, with 30-day volatility in markets such as the FTSE 100, EURO STOXX 50 and Swiss Market Index nearly doubling from February levels. This reflects a shift towards a more risk-off environment, as geopolitical tensions and inflation concerns drove a reassessment of risk across markets.