November 2024 Market Overview

November was characterised by robust U.S. equity performance, influenced by political developments and central bank policies. European and Chinese markets declined amid trade policy concerns. The U.S. dollar experienced significant strengthening, while the Federal Reserve and Bank of England each cut rates by 25 basis points.

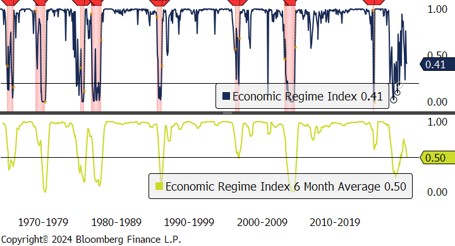

The Economic Regime Model shows volatility since early 2022, with September–October readings near 0.4 indicating weak but non-recessionary conditions. The six-month rolling average peaked in May 2024 and has since declined, signalling momentum loss that could affect equity markets going forward.

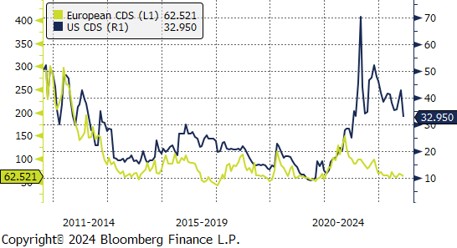

U.S. and European credit risk both declined in November. While U.S. credit risk remains elevated historically, the continued narrowing of spreads suggests regional stabilisation and improving confidence in financial system resilience.

Interesting

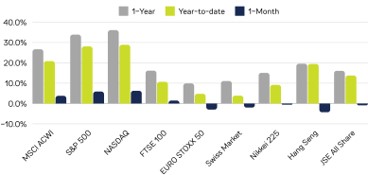

Gold delivered a 28% year-to-date return alongside a similarly strong performance from the S&P 500. Gold's gains reflect a confluence of geopolitical tensions, safe-haven demand, central bank diversification purchases and Fed rate cuts — a unique and complex market environment where both risk assets and traditional safe havens advanced simultaneously.

Performance

U.S. indices led global markets in November with month-to-date returns of 6.3% and 5.9%, demonstrating continued strength and sustained investor optimism in American markets. Global peers displayed mixed results, with non-US markets generally lagging as dollar strength and trade policy uncertainty weighed on international returns.

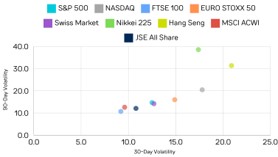

30-day volatility trends were mixed in November. The Hang Seng and Nikkei 225 experienced declining short-term volatility, while the S&P 500 and NASDAQ registered increases, reflecting the post-election repricing of risk in U.S. markets and the rotation into domestic-focused sectors.