October 2024 Market Overview

Global stock markets faced declines, with European indices particularly affected. Bond markets proved equally challenging, with Bloomberg's Global Aggregate recording one of its weakest performances in two years. Contributing factors included fiscal policy concerns, inflation persistence, and geopolitical tensions. Precious metals and energy commodities were notable outperformers.

October saw the world's political landscape in focus, with the US election dominating market attention. Our processes are evidence-based, leading us to observe changes in market structures as they unfold rather than positioning ahead of uncertain outcomes.

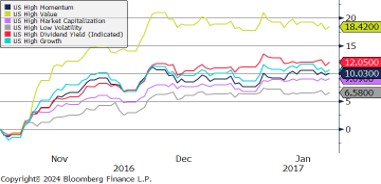

The chart above illustrates how different equity factors performed following Trump's 2016 election victory. However, we caution against assuming these patterns will repeat — we find ourselves in a very different fiscal, monetary, liquidity and geopolitical environment than in 2016.

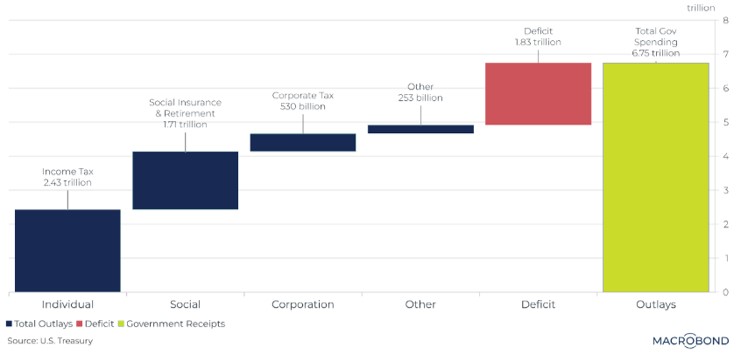

Despite differences between candidates' policy agendas, both indicate that fiscal deficits are set to persist. The 12-month rolling comparison of government receipts versus outlays reveals a structural deficit that transcends party preferences — a crucial secular force for markets to navigate.

US CDS spreads rose from 39.9 to 42.9 basis points during October while European spreads declined to 65.4, reflecting diverging perceptions of risk across regions as markets priced in election uncertainty and differing economic trajectories.

Performance

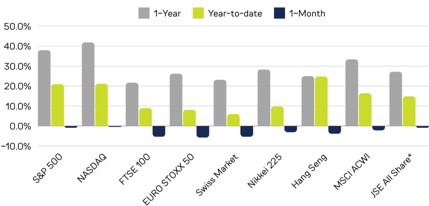

October delivered broad-based equity declines. The FTSE 100, Euro Stoxx 50 and Swiss Market each fell over 5% in USD terms, reflecting the combination of a stronger dollar, geopolitical headwinds and pre-election uncertainty weighing on international markets.

Volatility increased across most indices in October compared to September. The Hang Seng's volatility nearly doubled month-over-month as the initial euphoria from China's stimulus announcement faded and markets reassessed the sustainability of the rally.